There are 3 aspects to contribution: Make or buy analysis, contribution costing, absorption costing

Make or buy

- Should you make a component, or outsource it?

- based on what is more cost effective (because tooling can be expensive, but you don’t want to pay extra for components when you outsource (because suppliers are looking to profit on components))

Factors affecting Make or Buy Decisions

- If the business has enough labour and capacity to produce components in house

- If the business has expertise to make products in house

- If the supplier is reliable or not, and can produce high quality products quickly

- Small businesses are not a priority for suppliers (this can result in increased prices and long delivery times)

- How much control the business needs/wants on a particular component

Contribution Costing

Cost center: Admin, HR, Marketing, Technical Support, R&D. Cost centers are parts of a business that aren’t making them money directly (so these people are more likely to be laid off, if the company needs to reduce it’s cost center spendings)

Cost center: Admin, HR, Marketing, Technical Support, R&D. Cost centers are parts of a business that aren’t making them money directly (so these people are more likely to be laid off, if the company needs to reduce it’s cost center spendings)

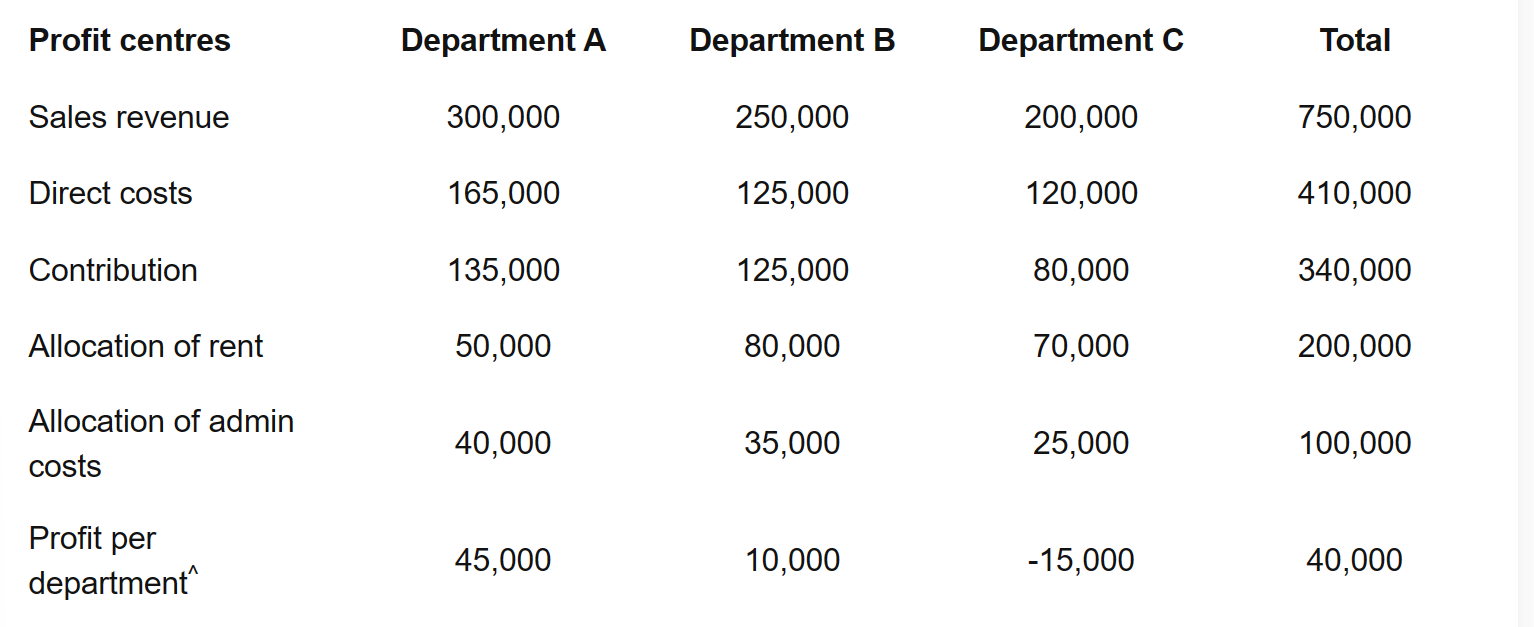

Absorption Costs

A way of finding the cost of a product by considering indirect expenses (overhead costs) and direct costs (cost of sales)

- Can be used to determine the cost profit per department (i.e. split overhead costs, like rent, based on the floor size. Then see which departement makes the most profit, given the overhead costs per department)

Note that: allocating overhead costs to each department can be random and subjective, so absorption costs may be inaccurate

Note that: allocating overhead costs to each department can be random and subjective, so absorption costs may be inaccurate