Depreciation is recorded in profit and loss account as a business expense. Also on the balance sheet “to reflect the fall in the market value of the asset”

you can sell depreciated assets for their residual value. Some times the residual value is 0

There are two ways to measure depreciation

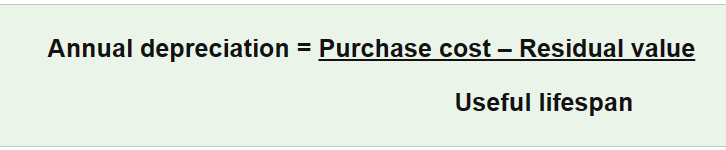

straight line method

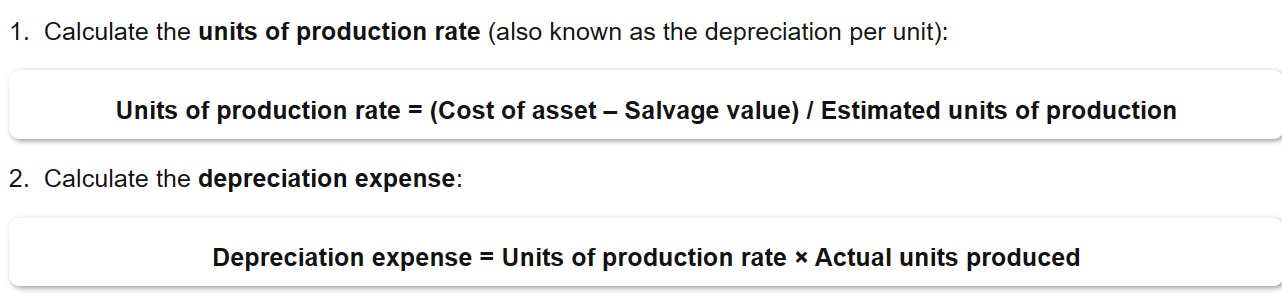

units of production method

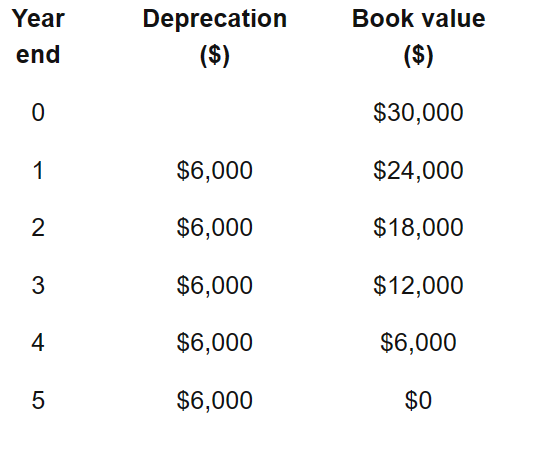

Straight line method

the value of the asset falls by the same amount each year

Advantages

easy to calculate

good for assets that have a known shelf life (like batteries or cereal)

Accurate for assets that are used regularly (i.e. furniture) over their lifetime

Easy for historical comparisons of data, since the depreciation value is the same each year

Disadvantages

Not all assets depreciate uniformly (i.e. cars depreciate the most right when you drive away with them)

Assets do not depreciate uniformly because they have higher repair/maintenance costs (i.e. cars, machinery)

Not suitable if you cannot estimate the life span of the product

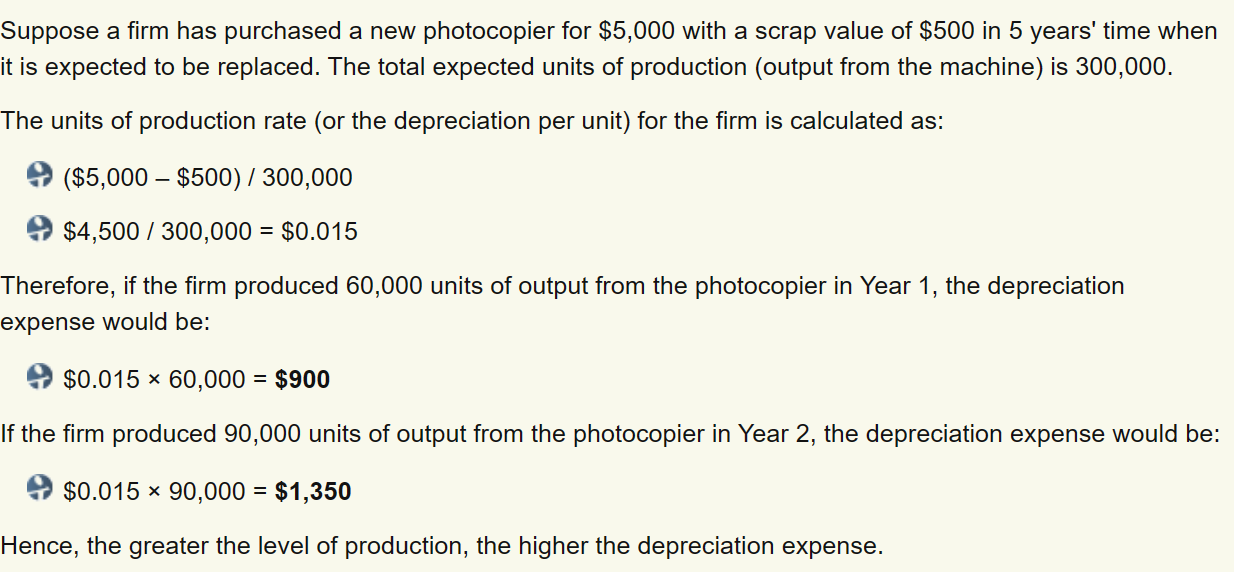

Units of production method

calculates depreciation based on usage of an asset

so a car would depreciate more if you drive more km on it

units of production means the expected output from the machine

Advantages

more accurate to use this method

More accurate for non-current assets that depreciate due to wear and tear, not just passage of time